投資就這樣而已,2個重點:

1. 挑高ROE的公司,便宜買,一路抱到貴了才賣

2. 依GDP按表操課加減碼

Investment is just that simple, with two key points:

1. Choose companies with high ROE, buy them when they are cheap, and hold them until they become expensive before selling.

2. Adjust your position according to GDP movements.

其它不要想太多,投資做不好多半因爲想太多,

這是巴菲特神功最難學成的一段!

Don't overthink things. If you struggle with investing, it may be because you're overanalyzing. This is the most challenging aspect of Buffett's skillset !

一般人常犯了不自覺的毛病,若我未指出必未察覺,

看長做短,

號稱要來學巴菲特卻每天盯著短線指標殺過來殺過去。

股票要做長做短皆可,但切勿混為一談,

犯了看長做短的錯誤,股票會抱不住。

Many investors unknowingly make mistakes that they're not aware of, and if I don't bring them to attention, they may not even notice. They tend to focus on short-term gains while claiming to learn from Buffett, constantly trading based on short-term indicators. Stocks can be held for the short or long term, but it's important not to confuse the two. If you make the mistake of treating short-term investments as long-term ones, you may not be able to hold onto the stock for very long.

我中碳8年賺6倍,8年之中,

經歷過多次的營收,甚至獲利衰退。

若每個月追蹤營收,將抱不了8年賺不了6倍。

I earned six times my initial investment in China Steel Chemical over the course of eight years. During that time, I experienced fluctuations in sales and even periods of declining profits. However, if I had focused solely on tracking its monthly sales, I may not have been able to achieve that six-fold return over eight years.

台股比較特殊,規定上市櫃公司每月要公布營收,

所以大家都緊盯著營收看。

我問強調要看營收的同學

「營收要怎麼追蹤,成長的好或衰退?」

同學答「廢話!當然成長的好。」

「可是我買股票多半買在衰退。」我冷回,

同學愣了一下,以為我連營收都不會追蹤才說出買在衰退,

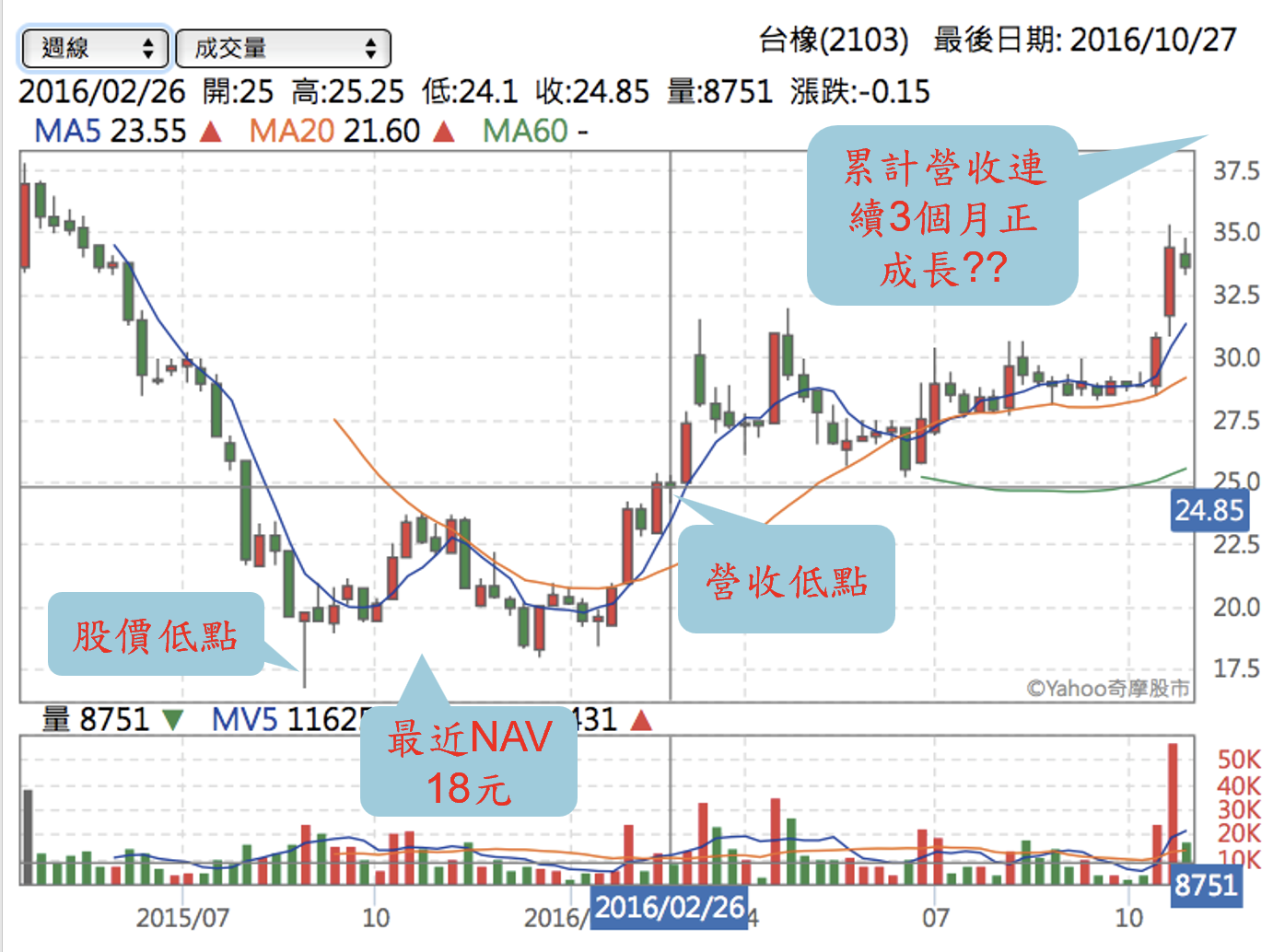

還教我怎麼追蹤「要等到營收動能出來,

累計營收連續3個月正成長時才可以買進。」

「是嗎?」我秀這張圖給他看

「台橡股價低點離何者比較近?」

絕對不是累計營收3個月正成長!

等到累計營收連續3個月正成長,股價早就漲翻天了。

In Taiwan, listed companies are required to disclose their monthly sales, making it a crucial factor for investors. I once asked a student who believed that monthly sales should be monitored closely, "How do you track sales, and which is better, growth or decline?" The student replied, "Of course, growth is better." However, I coldly pointed out that I had bought stocks mainly because sales had fallen. The student was momentarily stunned, thinking I didn't even know how to track sales by buying the dip.

He proceeded to teach me how to track sales, saying that I should only buy when there has been a strong growth in cumulative sales for three consecutive months. I then showed him a picture and asked, "Which is closer to the stock price low of Taiwan Synthetic Rubber (2103.TW)?" It certainly wasn't a three-month cumulative sales growth, as the stock price had risen during that period.

我跟那位教我看營收的年輕人說

「我1991年當分析師的第一天就知道看營收,

我在追蹤營收時你還在地上爬咧。」

我們這把年紀的人老愛拿歲數出來壓人。

When the young man who tried to teach me how to track sales, I told him, "I've been monitoring sales since my first day as an analyst in 1991. You were just a baby crawling on the ground back then." As someone who's been in the industry for a long time, I tend to count the number of years of experience I have.

我買CALM時公司獲利很好,ROE45%,

不久蛋價大跌,公司出現虧損,

連續4季營收、毛利率和季報都很難看,

跌到36元股價最低時有同學叫我賣,

我絲毫不為所動,因它產業地位沒變,

它是美國最大雞蛋商,市占率23%,

後來因為缺蛋股價大漲。

When I purchased shares in Cal-Maine Foods (CALM), the company was making considerable profits with an ROE of 45%. However, the price of eggs rapidly declined, causing the company to suffer losses. For four consecutive quarters, sales, gross margins, and quarterly reports were very poor. When the stock price hit a low of $36, a student suggested that I sell my shares. However, I decided to hold on to them because the company's position in the industry had not changed. It is the largest egg producer in the United States, with a market share of 23%. Its stock price later surged due to an egg shortage.

追蹤營收、 毛利率、季報看不了太遠,

檢定公司有沒有變才是重點。

While tracking revenue, gross profit margin, and quarterly reports are important, they may not provide a long-term perspective. t is more important to focus on the endurance of the company.

投資千萬不要想太多,否則會買不下去,

因底部都是利空充斥。

Don't overthink, or you'll end up hesitating. The market bottom is often accompanied by bad news.

2008年我在40元時買台化,當時金融風暴方殷,

營收衰退,單季出現虧損,

還傳出中東產油國煉油廠產能開出來,

成本比台塑集團低,

....利空一堆,烏雲罩頂。

後來股價漲到120元。

In 2008, I purchased shares of Formosa Chemicals & Fibre at NT$40 per share. During that time, the severe financial crisis caused a decline in sales and the company suffered losses for a quarter. Additionally, reports showed that new refineries had started production in Middle Eastern oil-producing countries, resulting in lower costs than Formosa Plastics Group. Despite these negative factors, the stock price eventually rose to NT$120.

買了才發現它面臨專利懸崖,

多數藥品專利權在未來幾年即將到期。

看國外研究報告建議都是「賣出、賣出、賣出」,

可是已經買了,只好硬著頭皮抱下去。

漲到70幾美元傳出輝瑞藥廠有意收購,

第一次出價它拒絕,二次調高價格又不要,

可是我要,就賣掉,剛好賣在最高價。

In late 2012, I purchased shares of the British pharmaceutical company AstraZeneca (AZN) for $47.5. Soon after buying, I discovered that the company was facing a patent cliff with many of its pharmaceutical patents expiring in the coming years. Despite foreign research reports advising to sell, I decided to hold onto my investment. Eventually, the stock price increased to over $70 and there were rumors of Pfizer planning to acquire AZN. Following AZN’s rejection of Pfizer’s first bid, Pfizer countered with a higher bid; however, AZN still turned it down. Contrary to AZN’s opinion, I liked the stock price level at the time, so I sold and it just happened that I sold at the peak.

前5大銀行通通跌破淨值,

工商、建設、農業、中行、交通,ROE都接近20%,

預期報酬率25%以上。

看到的人無不大讚甜美多汁,可是都不敢買,質疑呆帳太多。

大家不敢買,我就跳進去買中國銀行買在10多美元,

2015年大漲到17美元。

In the past few years, I have presented Chinese bank shares to my class. The top 5 banks have all fallen below their net assets. The ROE of Industrial and Commercial Bank, Construction Bank, Agricultural Bank, Bank of China, and Transportation Bank is close to 20% with an expected return of more than 25%. Everyone praised the juicy price, but they hesitated and questioned too much bad debt. I took the leap and bought Bank of China for more than $10. In 2015, it rose to $17.

我這番言論驚呆眾人,

非危言聳聽,有學理根據的。

My words shocked everyone.

This is not an exaggeration, but makes sense.

每次舊生來回鍋,都會關心他們股票做得如何?

幾乎百分之百無意外的,

績效好的都是一路抱,

不好的則跑來跑去。

Whenever my former students come back, I always inquire about their investment outcomes. Almost without exception, long-term investors have positive results, while poor performance is often attributed to speculators.

既然同學喜歡跑來跑去,我建議就不要跑了,

買了股票不用照顧,

這絕非在嘩眾取寵,實有所本。

Since many students prefer speculative trading, I recommend they stop trading and focus on long-term investments. By doing so, they don't have to constantly monitor their holdings. This advice is not meant to be sensational, but it is based on solid principles.

大家都知道我的賣股三原則:

1. 貴了

2. 壞了

3. 找到更好的。

Everyone knows my three principles for selling shares:

1. Expensive

2. Has gone bad

3. Find a better option

1. 貴了 和 3. 找到更好,大家都同意,

問題出在 2. 壞了,

發現公司變壞了要賣股多半來不及,股價早跌翻。

我買GNC,原來也覺得不錯,

推薦的同學說現代人注重養生會買一些補給藥品,

後來股價跌了原以為只是獲利衰退,

跌了9成才知負債不能展延,大誌大條。

同學問我要不要賣?

跌了9成,即便一天大跌20%對績效影響已不關痛癢,

股票跌多了有個好處,下跌空間就越有限。

Everyone agrees on the first and third principles of selling shares: 1. If it's expensive and 3. If a better option is available.

The second principle, "has gone bad," is often disputed as it's difficult to determine when a company has gone bad until it's too late and the stock price has already fallen significantly.

For example, I once purchased shares of GNC which initially performed well due to a student's recommendation that health supplements were in high demand. However, the stock price later declined, and I initially assumed it was only a decline in profits. It wasn't until the stock had fallen by 90% that I realized the company was unable to extend its debt and had gone bankrupt. When some students asked if I wanted to sell, I explained that the stock had already fallen by 90%, so even if it fell another 20% every day, it wouldn't significantly impact my overall performance. One advantage of stocks falling drastically is that the downside is limited.

照顧股票在照顧什麼?怕它變壞。

變壞了又通常來不及賣,

所以呢?就不要照顧啦。

What does taking care of stocks mean? It's being afraid that they will turn bad. When they do turn bad, it's usually too late to sell. So, what should you do? Just don't take care of them.

把賣股三原則的 2. 壞了 拿掉,

不就變成股票買了之後,不必停損,不必照顧,

一路抱到貴了才賣。

Remove the second principle of "2. Has gone bad" and it turns out you don't have to cut your losses or take care of it after purchasing. Hold onto it until the price becomes expensive.

我也實際去執行給大家看,

我的美股踩到很多地雷股,都未設停損,

VALE和GNC都曾跌了90%,

BBBY和VIAB跌60%,

HLF和TSCDY跌50%,...

可是總績效仍不錯,因多種果樹。

I proved this principle through my portfolio, which included some landmine stocks that I did not cut losses on. For example, VALE and GNC dropped by 90%, BBBY and VIAB fell 60%, and HLF and TSCDY fell 50%. However, due to diversification, the overall performance was still good.

投資跟農夫播種一樣,一把稻苗灑出去,

不期待每棵稻苗都長大,

只要7成能結穗即可豐收。

Investing is comparable to a farmer sowing seeds. Just like how a farmer scatters a handful of rice seeds, investors don't anticipate every single investment to yield returns. Instead, they aim for around 70% of their investments to mature and produce a bountiful harvest.

投資沒辦法百分百都對,

只要對個7成即會大賺,

講稿12/21提及買錯股機率約30%,

顛倒來看選對股的勝算為7成,

只要多種果樹,持續抱下去,當然會大賺!

Investing can't be 100% accurate, but getting it right 70% of the time can lead to substantial profits. In the speech on 12/21, it was mentioned that the probability of picking the wrong stock is about 30%, which means there's a 70% chance of picking the right one. By diversifying your investments and holding onto them consistently, you will certainly achieve significant gains !

講稿 1/21:歡迎 (Lecture 1/21 Welcome)- 講稿 2/21:知與不知 (Lecture 2/21 Knowable and unknowable)

- 講稿 3/21:巴六點 (Lecture 3/21 Buffett's Six Criteria)

- 講稿 4/21:物美價廉 (Lecture 4/21 Good quality and low price)

- 講稿 5/21:還原股價 (Lecture 5/21 Adjusted stock price)

- 講稿 6/21:高ROE (Lecture 6/21 High ROE)

- 講稿 7/21:配得出現金 (Lecture 7/21 High dividends)

- 講稿 8/21:會計 (Lecture 8/21 Accounting)

- 講稿 9/21:地雷股 (Lecture 9/21 Landmine stocks)

- 講稿 10/21:他們通通是錯的 (Lecture 10/21 They are all wrong)

- 講稿 11/21:不會變的公司 (Lecture 11/22 Durable)

- 講稿 12/21:多種果樹 (Lecture 12/21 Diversification)

- 講稿 13/21:IRR (Lecture 13/21 IRR)

- 講稿 14/21:殖利率陷阱 (Lecture 14/21 Yield trap)

- 講稿15/21:GDP理論 (Lecture 15/21 GDP Theory)

- 講稿 16/21:全世界都成立 (Lecture 16/21 Globally applicable)

- 講稿17/21:不要想太多 (Lecture 17/21 It's not that deep)

- 講稿 18/21:玩融資期貨選擇權是悲劇的開始 (Lecture 18/21 Margin trading, futures and options are the beginnings of a tragedy)

- 講稿 19/21:基金太貴,不做代操 (Lecture 19/21 Funds are too expensive, don’t manage other's funds)

- 講稿 20/21:股債不是蹺蹺板 (Lecture 20/21 Stock debt is not a seesaw)

- 講稿 21/21:技術分析真荒謬 (Lecture 21/21 Technical analysis is ridiculous)

沒有留言:

張貼留言

注意:只有此網誌的成員可以留言。