以前看的財報是單獨報表,

關於轉投資的部分從業外投資收入認列進來。

投資收入一個科目卻包含很多東西,

長投、短投,不管有幾家子公司全部認列在裡頭,

它只是一個數字,子公司到底長什麼樣完全看不清楚,

單獨報表有個缺點很容易藏污納垢,

賣不掉的存貨、收不回來的爛帳全藏在子公司裡,

母公司的報表看來很漂亮,存貨下降,應收減少。

後來交易所規定上市櫃公司須公布合併報表。

The financial report previously reviewed was a non-consolidated statement, with subsidiary investments being recognized as non-operating investment income. Investment income is categorized as one account, but includes many items such as long-term and short-term investments, regardless of the number of subsidiary companies involved. However, this is just a numerical representation and the actual appearance of the subsidiary companies is unclear.

The disadvantage of a non-consolidated statement is that it is easily susceptible to concealing financial improprieties. Unsold inventory and uncollectible accounts receivable can be hidden within the subsidiary companies, making the parent company's report look attractive with decreased inventory and reduced accounts receivable. Later, the exchange required listed companies to issue consolidated financial statements.

所謂合併報表是把母公司跟子公司的會計科目

直接相加扣掉重複的部分,

不是按持股比例認列。

跟拍照一樣,單獨報表等於媽媽在拍獨照,

有幾個小孩子完全看不清楚。

合併報表則是媽媽和小孩在拍全家福照片,

這個小孩是跟前夫所生,持股僅5成,只能拍半身?

不是!一樣全身拍進來,扣掉重複部分,

合併報表等於在拍全家福的照片。

The consolidated statement refers to the combination of the accounts of both the parent company and subsidiary company, with the repeated parts subtracted directly, rather than recognized in proportion. Think of it like taking a picture. A non-consolidated statement is like a picture taken only of the parent company, while its subsidiary companies are not visible. In contrast, a consolidated statement is like a family portrait, where the parent company and its subsidiary companies are all captured in the same image. For example, even if a subsidiary company was created with the parent company's former spouse and only holds 50% of the shares, it is still captured in full in the consolidated statement. The redundant information is subtracted, and the consolidated statement is like a comprehensive family picture.

什麼公司要編合併報表?

持股50%上,或者有控制權的。

明碁對友達的持股只有10%,

若友達總經理由明碁在指派,就要編合併報表。

Which companies compile consolidated statements? Companies that hold 50% or more of the shares, or have control. BenQ only holds 10% of the shares in AUO. If the CEO of AUO is appointed by BenQ, a consolidated statement will be compiled.

合併報表怎麼編?看這個例子比較清楚。

假設母公司資產100元,負債0,淨值100元,

母:100=0+100

投資10元到子公司占股權50%,

子:40=20+(10+10)

子公司淨值20元,負債20元,資產40元。

How to compile a consolidated statement? This example should provide clear insight.

The parent company holds assets worth $100, with no liabilities, resulting in net assets of $100.

Parent Company: Assets = Liabilities + Net Assets = $100 = $0 + $100

The parent company invested $10 in a subsidiary, representing 50% equity ownership.

Subsidiary: Assets = Liabilities + Net Assets = $40 = $20 + ($10 + $10)

The subsidiary's net assets stand at $20, with liabilities at $20 and assets worth $40.

合併資產就是直接相加扣掉重複的部分,

100+40然後呢?要扣掉10元,

這10元是母公司丟進來的,重複計算,

合併資產130元。

Consolidating assets involves directly adding and subtracting duplicate parts.

For example, if you add $100 and $40 and then subtract $10,

the $10 was invested by the parent company and was counted twice.

Therefore, the consolidated assets amount to $130.

合併負債0+20=20,未重複,

合併淨值則為110,

在合併淨值底下多一個科目少數股權10元,

來自持股50%以上子公司貢獻的部分。

Consolidated liabilities equal $0 + $20 = $20, without duplication.

The consolidated net assets amount to $110.

Under the consolidated net assets, there is a minority interest account of $10,

which represents the portion contributed by a subsidiary that holds more than 50% equity ownership.

損益表也是,把母公司跟子公司的所有會計科目

直接相加扣掉重複的部分,

到最後就是合併淨利,

底下一樣多一個科目叫少數股權。

The same applies to the income statement. All accounting entries from both the parent company and subsidiary are directly added and duplicates are subtracted. The bottom line is consolidated net profit. As in the case of net assets, there is a minority interest account included in the consolidated income statement.

在合併淨值跟合併淨利底下了多一個少數股權,

一張報表若搞不清到底是合併還是非合併?

找一下裡頭有少數股權的即合併報表。

In both the consolidated net assets and consolidated net profit, there is an additional account for minority interests.

If you are unsure whether a statement is consolidated or non-consolidated, look for the presence of the minority interests account.

If it is included, the statement is a consolidated one.

報表有2種,算出來答案要一樣,

ROE若拿單獨報表來算,直接就是EPS÷NAV,

若拿合併報表來算,就得再扣掉少數股權。

There are two forms of statements, and the outcome must be consistent. If ROE is computed using a non-consolidated statement, it is directly EPS÷NAV. On the other hand, if a consolidated statement is used for calculation, we need to subtract minority equity.

盈再率的計算,因為合併報表僅針對

合併淨值跟合併淨利區分少數股權,

其他的科目就沒有這樣的區分,

無合併固定資產的少數股權與合併長期投資的少數股權。

若拿合併報表來算,請全部用合併的去算。

The calculation of PR% uses consolidated statements, which only distinguish minority interests in consolidated net assets and consolidated net profit. There is no such distinction in other accounts, such as consolidated fixed assets and long-term investments without minority interests. When using consolidated statements to calculate PR%, it is necessary to include all consolidated figures.

盈再率用合併報表跟非合併算會有差異,

何者比較大?

不一定,子公司資本密集的公司比較多

用合併報表算出來的盈再率比較大。

The calculation of PR% using consolidated statements and non-consolidated statements may result in different outcomes, but it is not certain which one is greater. Companies with more capital-intensive subsidiaries tend to have a higher PR% when calculated using consolidated statements.

講稿9/21提到地雷股被嚴重掏空的標準,盈再率大於200%,

在合併報表仍然適用。

目前收集到國外地雷股的例子,

江西賽維、玖紙協鑫、中國伊利,盈再率都超過200%。

IIn the 9/21 lecture, the criteria for severely hollowed-out landmine stocks was discussed as having a PR% greater than 200%. This criterion still applies when using consolidated statements. Currently, examples of foreign landmine stocks have been collected, including Jiangxi LDK Solar, Nine Dragons Paper, and China Yili, whose PR% have all exceeded 200%.

49國的盈再表抓的都是合併報表。

The tables of 49 countries in "On" now all use consolidated statements.

盈再表有時候需要修改,

券商資料庫格式更動,盈再表就得跟著改,

改好之後會在討論區張貼公告,

不用擔心我們這堂課是永久保固,盈再表也是。

大家應該知道這一輩子已脫離不了我的魔掌心了,

所謂做投資?就在按盈再表而已,

同學問我哪一支股票怎麼看?

我也是根據盈再表在解釋。

On's table may need to be updated from time to time,

due to changes in the format of the broker's database.

When updates are made, a notice will be posted in the discussion forum.

Please be assured that our class and On's table are both covered by a permanent warranty.

You should be aware that you will never escape my influence for the rest of your life.

What is investment all about? Simply consult On's table.

When students ask for my opinion on certain stocks,

I always base my explanation on On's table.

把投資變簡單的人,不是巴菲特,是我啊!

有盈再表之後投資才變得這麼簡單,

盈再表是我寫的程式,非常複雜的程式。

The person who made investment simple is not Warren Buffett, it's me!

Investment only became this simple with the existence of On's table, which is a program written by me and is extremely complex.

同學下載了新版的盈再表,

請把舊版的刪掉,保留新版的就好,

看有些人還在收集舊版的盈再表,

是想來換公仔嗎?

If students have downloaded a new version of On's table,

it is recommended that they delete the old version and retain the new one.

Some students have saved previous versions of On's table.

Would they like to exchange them for toys?

同學還問我新版和舊版數字為何會不一樣?

就是不一樣才要更新啊!

Students also ask me why the numbers in the new version and the old version are different.

This is the reason for update !

上這堂課常常被同學問到一些讓我全身無力的問題。

報名時同學說他老婆對投資也很有興趣,

他願意幫老婆付中午便當的錢,

問我這樣子可不可以?

我回他「唉喲!這樣怎麼好意思呢,

可是你老婆還是要再給我學費呀!」

In this class, I'm often asked some questions that leave me feeling powerless by students.

On the first day of class, a student mentioned that his wife was also interested in investing and offered to pay for her lunch. I replied, "Oh, how thoughtful! However, your wife still needs to pay the tuition fee."

另外一個同學問,他老爸對投資也很有興趣,

他想把他一次永久免費保固的機會讓給老爸可不可以?

我說「吃到飽的餐廳兩人同來也是收2個人的餐費啊!」

Another student asked if he could transfer his chance for a free permanent warranty to his father, who is also interested in investing.

I responded by saying, "Even if two people dine together in an all-you-can-eat restaurant, each person still has to pay for their own meal."

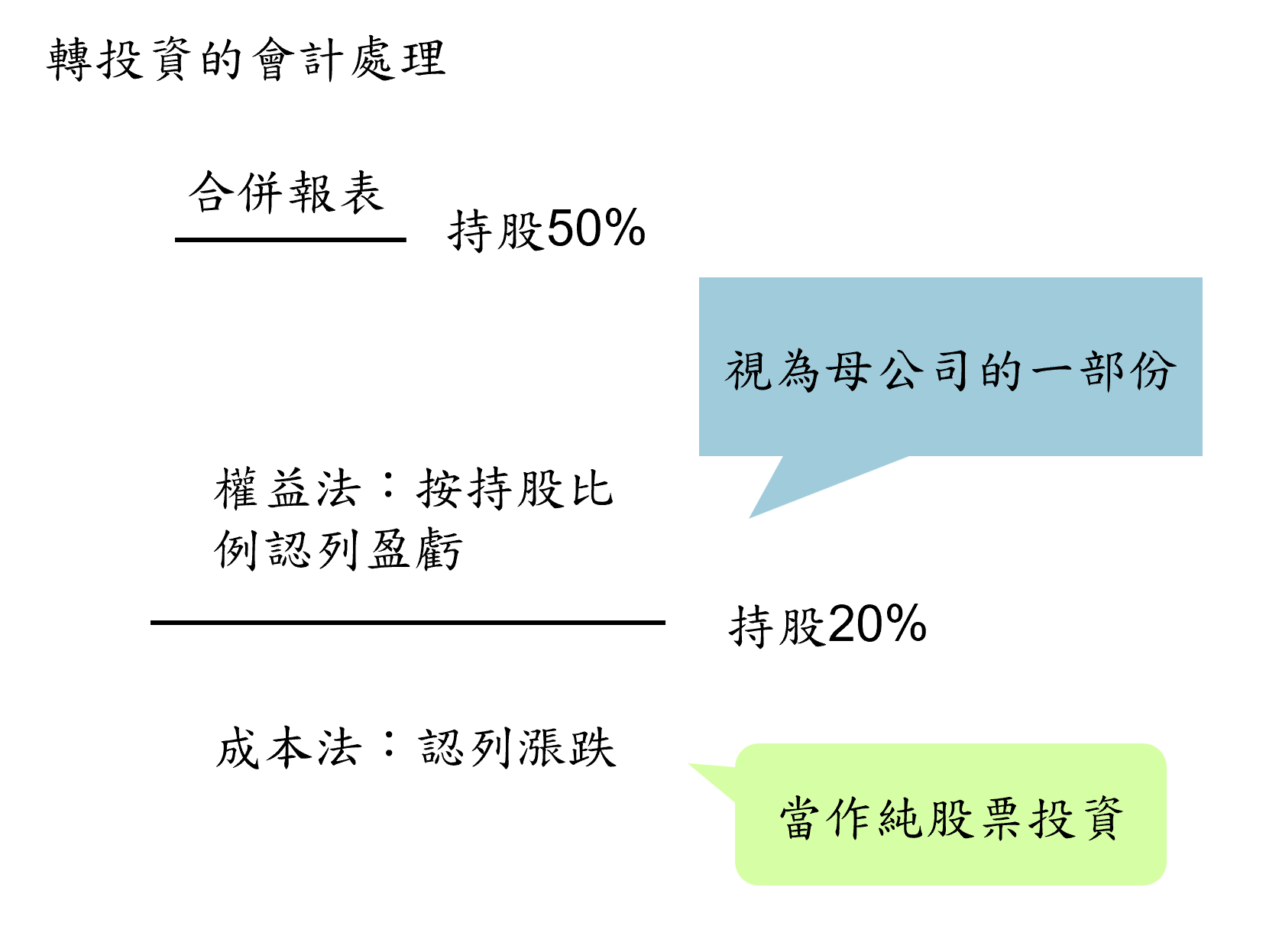

投資的會計處理:

公司投資另外一家公司在會計上要去怎麼記帳?

這裡牽涉到一些專有名詞,同學要努力記一下,

以後看到相關報告時才知道什麼意思。

Investment accounting:

How does the company keep books when it invests in another company ?

There are some terminologies involved here, please try hard to remember.

You will know what it means when you see the relevant report later.

轉投資怎麼記帳?以持股20%為準,

20%以上的,50%以下叫做權益法,

按持股比例認列盈虧。

20%以下為成本法,認列股價漲跌。

為何如此區分?

20%以上視為公司的一部分,

即便沒配息出來,仍直接按持股比例認列盈虧。

20%以下成本法則當作純粹的股票投資,

認列股價的漲跌。

How to record investment in financial statements? A 20% shareholding is taken as a baseline. Investments above 20% but below 50% are accounted using the equity method, where profit and loss are recognized based on the proportion of shareholdings. Investments below 20% are accounted using the cost method, and any changes in stock price are recognized. Why the distinction? Investments exceeding 20% are considered part of the company, and the profit and loss are recognized directly based on the shareholding ratio, even if no dividends are distributed. In contrast, investments below 20% using the cost method are considered a pure stock investment, and fluctuations in stock price must be recognized.

舉例說明,權益法:持股20%的子公司賺了25元,

在母公司損益表業外投資收入增加5元,

資產負債表長投增加5元,現金未增,因只是認列。

Example of Equity Method: A subsidiary with 20% shareholding earns a profit of $25.

The parent company's non-operating investment income on the income statement increases by $5.

The long-term investments on the balance sheet also increase by $5, but cash does not change as this is a bookkeeping entry only.

當子公司配息3元,則視為投資收回,

母公司現金增加3元,長投減掉3元,因視為投資收回。

這跟有些人說他股票抱好幾年了,

每年配息把持有成本扣掉,持股已是零成本,

即視為投資收回。

When a subsidiary pays a dividend of $3, it is considered a return on investment. The parent company's cash increases by $3, and the long-term investment decreases by $3 as it is considered a return on the investment. This is similar to long-term investors, where the annual dividends minus the holding costs equal zero, resulting in a return on investment.

有人問,長投減3元,減到最後長投會不會變成負的?

不會,長投頂多變成0,因為公司賺5元,長投即增加5元,

配息頂多5元,長投減到最後只會變成0,不至於變成負的。

A question was raised if the reduction of long-term investment by $3 would result in a negative value. The answer is no, the long-term investment will only decrease to 0 at the most. This is because the subsidiary earned a profit of $5, and the long-term investment increased by $5. The dividend received can only be a maximum of $5, so the long-term investment will only decrease to 0, and it will not become negative.

成本法認列股價漲跌,分為交易目的跟備供出售,

交易目的是做短線的股票,

備供出售就是可供出售,為做長線的股票。

The cost method recognizes changes in stock prices, which can be classified into two categories: transaction purposes and available for sale.

Transaction purposes refer to stocks held for short-term purposes, less than a year.

Available for sale refers to stocks held for long-term purposes.

交易目的股價漲跌在業外的金融資產評價科目認列,

賣掉股票則記為處分利得。

Stock price rises and falls of transaction purpose are recognized in non-operating financial asset evaluation account.

Sale of stocks is recorded as a disposal gain.

永記在以往每季賺 1 億多元,

2012年第一季卻賺了3.1億元,

其中 1 億多元金融資產評價利益,

因為該季股市大漲從6,600漲到8,200。

永記是做油漆的,本業還算賺錢,

可是未全配息給股東,

還留下一些錢自己在玩股票,股票玩得很大。

Yung Chi Paint (2726.TW) has been earning more than NT$100 million in profit every quarter in the past, but in the first quarter of 2012, it earned NT$310 million. Among them, more than NT$100 million was financial asset appraisal income, due to the surge in the stock market from 6,600 points to 8,200 points this quarter. Yung Chi is a painter and his main business is making money. However, dividends are not fully paid to shareholders, and some money is left for the manager to play stocks, which is a big play in the stock market.

備供出售的股價漲跌不認列損益,改在淨值調整。

The stock price changes for available-for-sale securities are not recognized as gains or losses and are instead adjusted in the net assets.

新光金2011年淨利賺了55億元,可是淨值減少174億元。

新光金是壽險公司,投資很多股票,

2011年壽險本業仍然賺錢,

可是股市空頭,指數9,200跌到6,600,

股票賠了錢列為備供出售,

跌價損失不用提列損失,從淨值扣掉,少掉174億元。

這跟一個人薪水10萬元,玩股票賠了300萬元一樣,

究竟賺錢還是賠錢?

Shin Kong Financial Holding (2888.TW) reported a net profit of NT$5.5 billion in 2011 despite a decrease in its net assets by NT$17.4 billion. As a life insurance company, Shin Kong heavily invests in stocks. Although its life insurance business remained profitable in 2011, the stock market was in a bear market, declining from 9,200 to 6,600 points. The capital losses were recorded as available for sale, but they are not considered actual losses, but rather a reduction in net assets, which were NT$17.4 billion. It's like someone who has a salary of $100,000 and loses $3 million in stock trading. Does he make money or lose money ?

潤泰全2015年EPS 8.1元,隔年股息僅1.6元,

為何配息僅20%這麼少?

因為認列轉投資南山人壽備供出售損失。

潤泰全2015年淨值少了802億元,少了71%。

若非2013年辦了現金增資,2015年淨值將成負數,破產!

Ruentex Industries (2915.TW) had an EPS of NT$8.1 in 2015, but the dividend for the following year was only NT$1.6. Why is the dividend payout ratio so low at only 20%? A loss in Nanshan Life was confirmed, resulting in a loss on available for sale, causing a decrease in Ruentex Industries' net assets in 2015 to NT$80.2, a decrease of 71%. If it weren't for the right issue in 2013, the net assets in 2015 would have become negative and the company would have gone bankrupt.

備供出售的跌價不計損失,盈餘虛增,

從淨值調整,淨值下降,

將造成ROE上升,內在價值增加,這豈不矛盾?

其實不會,價值仍然減少,

內在價值是根據股息折現公式算出來的,

這條公式講稿15/21講到股票的貴淑價時會詳細解釋。

股票賠錢配不出股息,

淨值減少賣出價下降,

所以根據公式算出來的內在價值將減少,不會增加,

並不矛盾!

Fall in available-for-sale prices is not included in loss and exaggerates profits. However, after adjusting the net assets, the net assets decrease, which may result in an increase in ROE and perceived intrinsic value. But in reality, the intrinsic value decreases. The intrinsic value is calculated using the dividend discount model, which will be explained in more detail in lecture 15/21. The decrease in capital leads to a lack of dividends, a decrease in net assets, and a decrease in selling prices, resulting in a decrease in intrinsic value calculated by the formula, rather than an increase. There is no contradiction.

成本法公司配息計為股利收入,

和投資收入同一個科目。

投資收入科目包含了權益法的盈虧和成本法的股息。

The cost method combines dividend income and investment income into a single account. The investment income account includes both the profit and loss of the equity method and the dividends of the cost method.

還有一個名詞大家需要了解,商譽,不是公司的名譽,

而是合併時產生的會計科目,

用比較高的成本合併另一家公司時即產生商譽。

There is another term that everyone needs to understand, goodwill. It is not a company's reputation, but rather an accounting account created during mergers and acquisitions. Goodwill is generated when another company is acquired at a higher cost.

合併分為現金收購和換股合併。

Mergers are divided into cash acquisitions and stock-swap mergers.

現金收購A和B這兩家公司,

A公司 資(10)=債(2)+值(8)

B公司 資(9)=債(3)+值(6)

Cash acquisition of Companies A and B:

Co.A A(10) = L(2) + E(8)

Co.B A(9) = L(3) + E(6)

A公司花7元收購B公司淨值6元。

收購之後A公司的資產負債表變成左邊的現金少7元,

無形資產增加 1 元商譽。

A(B) 資[10+9-7現金+無形(+1商譽)]=債(2+3)+值(8)

Company A invested $7 to acquire Company B, which had net assets of $6. Following the acquisition, the cash balance on Company A's balance sheet decreased by $7. The intangible asset account for goodwill increased by $1.

The balance sheet for Company A (post acquisition of Company B) is represented as follows:

A(B) A[10 + 9-7 cash + intangible (+1 goodwill)] = L(2 + 3) + E(8)

換股合併,一樣是A跟B這兩家公司,

換股合併股權各占一半,合併成本7元(=(8+6)/2)),

合併B公司淨值6元,

合併之後A公司的資產負債表左邊無形資產增加1元商譽,

右邊淨值的資本公積增加 1 元發行溢價。

A(B) 資[10+9+無形(+1商譽)]

=債(2+3)+值[8+6+資本公積(+1發行溢價)]

謝謝吳朝同會計師、陳新元桑、郭東嶂桑指導。

In a stock-swap merger between Companies A and B, each company will have half of the combined equity. The cost of the merger is $7 (calculated as (8+6)/2). The net assets of the merged Company B is $6.

After the merger, the intangible asset account for goodwill on the balance sheet of Company A will increase by $1. The capital surplus of net assets on the right-side of the balance sheet will also increase by $1 due to the issuance premium.

The balance sheet for Company A (post merger with Company B) is represented as follows:

A(B) A[10+9+intangible (+1 goodwill)] = L(2+3) + E[8+6+capital surplus(+1 issue premium)]

I would like to express my gratitude to Accountants Chaotong Wu, Sinyuen Chen, and Dongzhang Guo for their guidance.

合併之後每年經過會計師的精算,

發現子公司的價值低於其淨值時,須認列商譽減損,

且一次提列,不能再沖回。

Following the merger, the accountant performs an annual actuarial calculation. If the value of the subsidiary is determined to be lower than its net assets, an impairment of goodwill must be recognized. This write-off is a one-time event and cannot be reversed.

商譽減損:子公司的價值低於合併成本

資(-商譽)=債+值(-損益)

Goodwill Impairment: When the value of the subsidiary is lower than the combined cost, the goodwill must be reduced. This results in the decrease of assets (A) and increase of profit and loss (E) in the balance sheet.

A(-goodwill) = L + E(-profit and loss)

我買GD沒多久晚上一開盤跌7%,很緊張,

按盈再表發現第四季虧損21億元,以往每季賺6億多元,

查新聞才知是提列子公司商譽減損。

一次提列股價一次反應。

Shortly after I acquired shares of GD, the opening price plummeted by 7% and I felt anxious. The 4th quarter results showed a loss of $2.1 billion according to On's report, compared to a profit of over $600 million in the previous quarter. Upon investigating, I discovered that the subsidiary had recorded a goodwill impairment charge. This led to a decline in the stock price after the write-off.

2013年宏碁也提列Gateway商譽減損,

那幾天股價大跌。

In 2013, Acer also recognized a goodwill impairment of Gateway, causing the stock price to significantly decrease.

同學會發現,我們買的股票常常會被人家合併,

因為我們看好,別人也看好,

我們覺得便宜,別人也是。

一旦被合併股票是賣或留?

以存續公司股價貴淑而定。

You will find that the stocks we invest in are often subject to mergers by other companies, because we have a positive opinion of the company and others share the same sentiment. We believe that it is as reasonably priced as the rest of the market. Whether the merged stock is sold or held onto depends on the valuation of the surviving company.

我買的DTV被AT&T用一股95美元合併。

雖然95美元對DTV而言是便宜的,可是AT&T貴。

當DTV股接近95美元利多反應完畢之後就該把DTV賣掉,

因轉換成AT&T股價也是貴了,一樣要賣掉。

The DTV stock that I bought was merged by AT&T at a price of $95 per share. Although $95 for DTV may seem like a good deal, AT&T is overpriced. When the stock price of DTV approaches $95, the bullish response will have been exhausted, and it would be wise to sell DTV. Since converting to AT&T stock is also too costly, it would also need to be sold.

講稿 1/21:歡迎 (Lecture 1/21 Welcome)- 講稿 2/21:知與不知 (Lecture 2/21 Knowable and unknowable)

- 講稿 3/21:巴六點 (Lecture 3/21 Buffett's Six Criteria)

- 講稿 4/21:物美價廉 (Lecture 4/21 Good quality and low price)

- 講稿 5/21:還原股價 (Lecture 5/21 Adjusted stock price)

- 講稿 6/21:高ROE (Lecture 6/21 High ROE)

- 講稿 7/21:配得出現金 (Lecture 7/21 High dividends)

- 講稿 8/21:會計 (Lecture 8/21 Accounting)

- 講稿 9/21:地雷股 (Lecture 9/21 Landmine stocks)

- 講稿 10/21:他們通通是錯的 (Lecture 10/21 They are all wrong)

- 講稿 11/21:不會變的公司 (Lecture 11/22 Durable)

- 講稿 12/21:多種果樹 (Lecture 12/21 Diversification)

- 講稿 13/21:IRR (Lecture 13/21 IRR)

- 講稿 14/21:殖利率陷阱 (Lecture 14/21 Yield trap)

- 講稿15/21:GDP理論 (Lecture 15/21 GDP Theory)

- 講稿 16/21:全世界都成立 (Lecture 16/21 Globally applicable)

- 講稿17/21:不要想太多 (Lecture 17/21 It's not that deep)

- 講稿 18/21:玩融資期貨選擇權是悲劇的開始 (Lecture 18/21 Margin trading, futures and options are the beginnings of a tragedy)

- 講稿 19/21:基金太貴,不做代操 (Lecture 19/21 Funds are too expensive, don’t manage other's funds)

- 講稿 20/21:股債不是蹺蹺板 (Lecture 20/21 Stock debt is not a seesaw)

- 講稿 21/21:技術分析真荒謬 (Lecture 21/21 Technical analysis is ridiculous)

沒有留言:

張貼留言

注意:只有此網誌的成員可以留言。